Dubai property sales hit AED 682.6 billion in 2025, with 267,499 transactions recorded across the year. Yet for most buyers — expats, nationals, and overseas investors alike — the mortgage process is the least understood part of the deal.

Most people know a mortgage means borrowing money secured against a property. What they don’t know is how UAE-specific rules work: how much deposit they actually need, what fees come on top, and what happens between signing a sales agreement and collecting a title deed.

This guide answers all of that, step by step. Whether you’re a salaried expat, a UAE national, or an overseas investor, here’s exactly how a UAE mortgage works.

Who Can Get a UAE Mortgage? Expats, Nationals, and Non-Residents

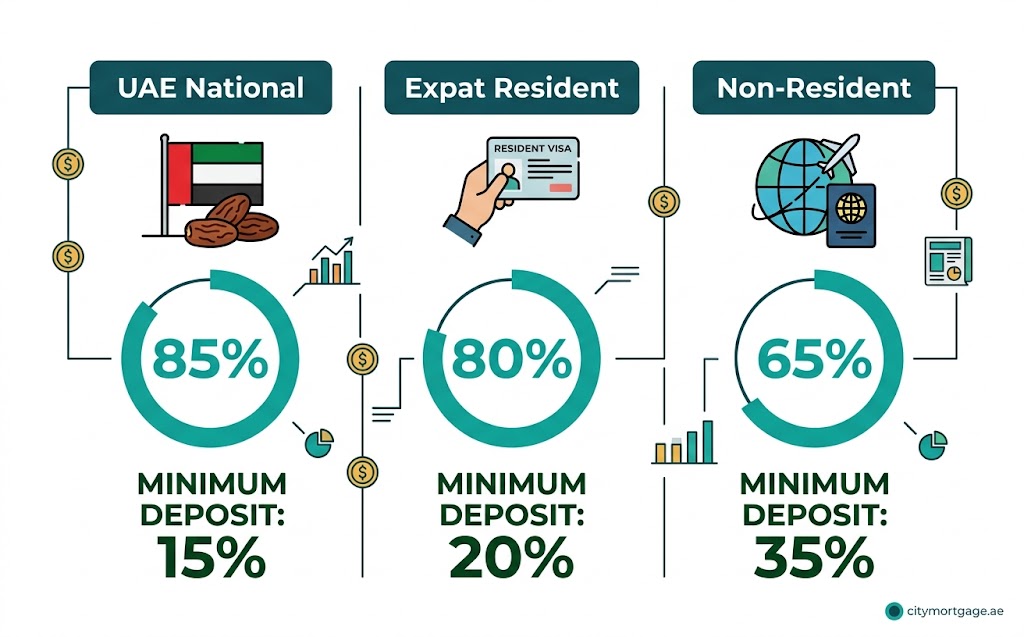

UAE mortgages are available to resident expats, UAE nationals, and non-resident international investors. Your residency status determines how much you can borrow, under CBUAE loan-to-value (LTV) regulations.

Here’s how LTV breaks down by buyer type for properties under AED 5 million:

| Buyer Type | Max LTV | Minimum Deposit |

|---|---|---|

| UAE Nationals | 85% | 15% |

| Expat Residents | 80% | 20% |

| Non-Residents | 65% | 35% |

For properties above AED 5 million, LTV limits reduce further. Nationals drop to 75%, and expat residents drop to 65%.

One important myth to clear up: non-residents can absolutely get a UAE mortgage. The conditions are stricter, and fewer lenders offer it, but it is a real and increasingly common route for overseas investors buying in Dubai’s freehold zones.

How Much Deposit Do You Really Need for a UAE Mortgage?

Expat residents need a minimum 20% deposit for properties under AED 5 million. UAE nationals qualify from 15%. Non-residents must put down at least 35% under CBUAE mortgage regulations.

On a AED 1.5 million property, that means:

- Expat resident: AED 300,000 minimum deposit

- UAE national: AED 225,000 minimum deposit

- Non-resident: AED 525,000 minimum deposit

For off-plan property, the rules differ. Most UAE banks won’t lend against off-plan until the property reaches a certain construction stage — typically 50% or more. Developer payment plans are often used in the early stages, with a bank mortgage arranged closer to completion. Don’t assume you can mortgage an off-plan purchase at the same LTV as a ready property without checking first.

As an independent broker, we regularly speak with first-time buyers who’ve already paid a 10% developer deposit on an off-plan unit — then discover their bank won’t mortgage it until 50% completion. That gap can be 18–24 months. If you’re buying off-plan, map your payment plan before you commit, not after.

What Are the Total Upfront Costs When Buying with a Mortgage in Dubai?

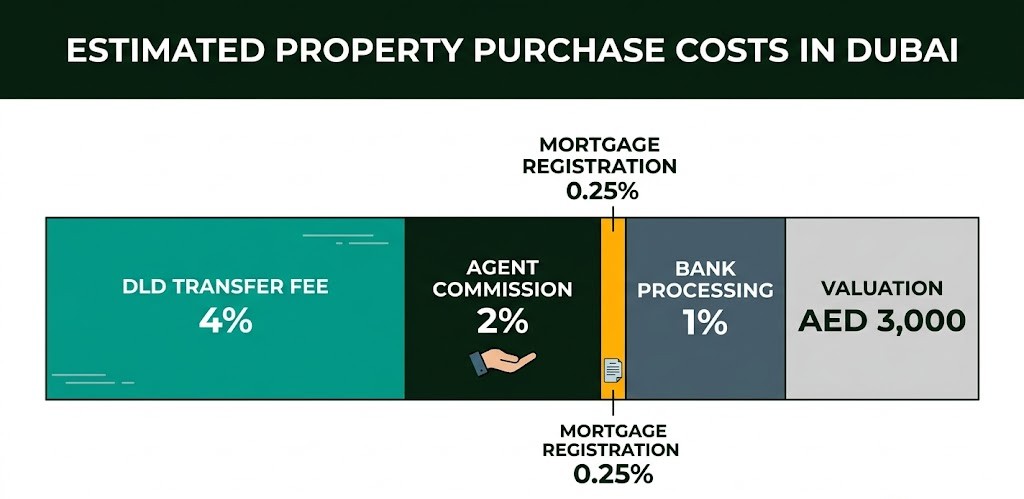

This is where buyers get caught out. The deposit is not the only large cost. When you buy with a mortgage in Dubai, you’re looking at roughly 6–7% of the purchase price on top of your deposit in day-one fees.

Budget 6–7% of the purchase price in upfront costs, separate from your deposit. On a AED 1.5M property, that’s AED 90,000–105,000 in fees alone before you touch the deposit.

Here’s the full breakdown:

| Cost Item | Amount |

|---|---|

| DLD transfer fee | 4% of property price |

| DLD mortgage registration | 0.25% of loan amount |

| Property valuation | ~AED 2,500–3,500 |

| Bank processing fee | ~1% of loan amount |

| Agent commission | ~2% of property price |

The DLD mortgage registration fee is a fixed government charge — currently 0.25% of the mortgage value, processed in 20–25 minutes at the DLD service centre. It is not negotiable and it cannot be rolled into your mortgage. The same applies to the 4% transfer fee.

Many buyers also forget the agent commission if they’re buying through a broker. Budget for all of these before signing anything.

Your UAE Mortgage Snapshot

Pick your buyer type and property price — your numbers update instantly.

Fees include: DLD transfer 4% · Agent commission 2% · Mortgage registration 0.25% of loan · Bank processing ~1% of loan · Valuation ~AED 3,000

Estimates follow CBUAE LTV guidelines and DLD fee schedule. Not financial advice. Actual approval depends on your income, credit profile, and lender policy.

What Is DBR and Does Your Income Actually Qualify?

DBR stands for Debt Burden Ratio. UAE banks cap it at 50% of your gross monthly income — meaning all existing debt repayments plus the new mortgage cannot exceed half your salary.

If you earn AED 25,000 per month, your total monthly obligations — car loan, personal loan, credit cards, and the new mortgage payment — can't exceed AED 12,500.

Banks calculate DBR differently for salaried and self-employed applicants. Salaried employees typically provide 3–6 months of payslips and bank statements. Self-employed professionals usually need 2 years of audited financials plus business bank statements. Credit card limits count against your DBR even if you don't use them — so it's worth reducing limits before applying.

In our experience, the most common reason UAE mortgage applications come back reduced isn't salary — it's credit card limits. Most buyers don't realise that an unused AED 30,000 credit card limit still counts against your DBR. We advise clients to cancel or reduce unused cards at least 30 days before applying.

How Does the UAE Mortgage Process Work, Step by Step?

Here's the full sequence from your first enquiry to getting a title deed.

Step 1 — Eligibility Check (1 day) Before anything else, verify your LTV, DBR, and credit profile via the AECB (Al Etihad Credit Bureau). An independent broker like City Mortgage does this free and gives you a realistic borrowing figure before you approach any bank.

Step 2 — Mortgage Pre-Approval (3–5 days) You submit your documents to a lender. They issue a pre-approval letter — a conditional offer confirming how much they'll lend. Pre-approvals are usually valid for 60–90 days depending on the bank.

Step 3 — Property Selection With pre-approval in hand, you search with a clear and verified budget. Sellers and developers take pre-approved buyers more seriously in negotiations.

Step 4 — Bank Valuation (1–3 days) Once you agree on a property, the bank sends their own valuer to confirm the market value. If the valuation comes in below the agreed purchase price, the bank lends against the lower figure — and you cover the difference in cash.

Step 5 — Formal Loan Offer (3–7 days) The bank issues a formal mortgage offer based on the valuation. Review the rate, tenure, early repayment conditions, and all fees before signing.

Step 6 — DLD Registration (1–3 days) The sale and mortgage are registered at the Dubai Land Department. The 4% transfer fee and 0.25% mortgage registration fee are paid at this stage via a trustee office.

Step 7 — Title Deed Issued The DLD issues the title deed in your name, with the mortgage noted on it. Repayments begin the following month.

Total timeline: 4–8 weeks for a straightforward ready-property purchase. Off-plan or non-resident applications often take longer.

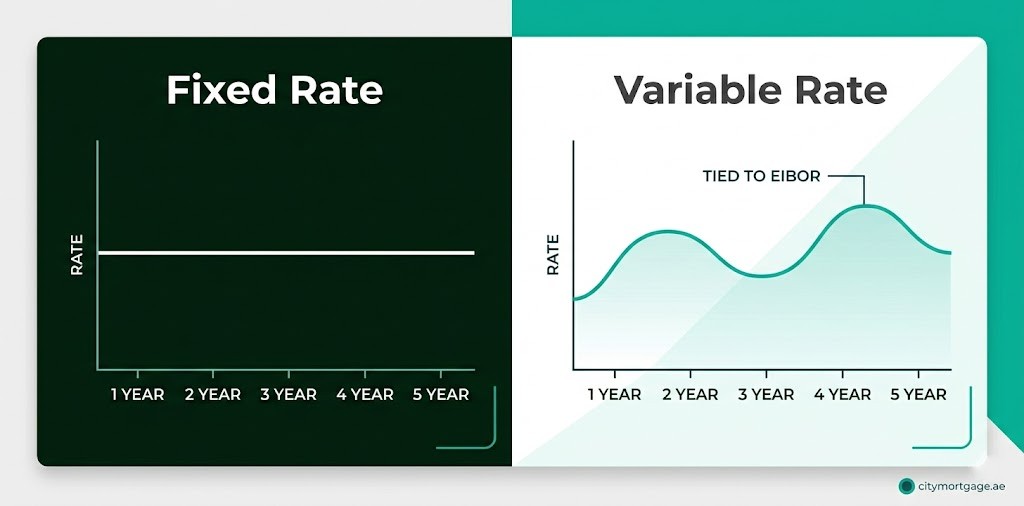

Fixed vs Variable Mortgage Rates — Which One Should You Choose?

UAE mortgage rates are either fixed for 1–5 years then variable, or floating from day one based on EIBOR. Current 1-month EIBOR sits around 3.64–3.72% (as of May 2026, per FCMB and Doha Bank reference rates). Major banks currently offer fixed rates from approximately 3.99% to 4.49%.

As a benchmark, FAB currently offers fixed rates from approximately 3.99% to 4.44% depending on tenure and salary transfer. Standard Chartered sits at around 4.13% to 4.49% for longer fixed periods.

Fixed rate suits buyers who want cost certainty in the first few years. Variable suits buyers who expect rates to fall or plan to sell or remortgage before the fixed window closes.

The mistake most buyers make is not reading what happens when the fixed period ends. At that point, your rate reverts to variable — typically EIBOR plus a bank margin. If EIBOR drops, your payment follows. If it rises, so does your cost. Ask your broker for the revert rate before signing.

Is Islamic Home Finance Different from a Conventional Mortgage?

Islamic home finance uses Murabaha or Ijara structures instead of interest. The practical difference is how profit is calculated — not necessarily what you pay each month. Islamic products are competitively priced against conventional options and are available to all buyers, not just Muslims.

Under a Murabaha arrangement, the bank buys the property and resells it to you at an agreed higher price, paid in installments. Under Ijara, the bank owns the property and leases it to you, with ownership transferring on final payment.

Don't assume Islamic finance costs more. Lenders like Dubai Islamic Bank and Abu Dhabi Islamic Bank price their products to compete directly with conventional rates. The right comparison is total monthly payment and lifetime cost — not the product label.

Frequently Asked Questions

Can expats get a mortgage in Dubai?

Yes. Expat residents can borrow up to 80% of a property's value for purchases under AED 5 million, under CBUAE regulations. Non-resident expats living overseas can also get a UAE mortgage, though the maximum LTV is 65% and fewer lenders offer this product. An independent broker can identify which lenders are actively approving non-resident applications.

What documents do I need for a UAE mortgage?

Salaried employees need: passport, UAE residence visa, Emirates ID, 3–6 months of payslips, 3–6 months of bank statements, and an employer salary letter. Self-employed applicants additionally need 2 years of audited accounts, a trade licence, and business bank statements. Non-residents need passport, overseas proof of income, and 6 months of international bank statements.

How long does mortgage approval take in Dubai?

Pre-approval takes 3–5 working days once documents are submitted. Full formal approval, including valuation and loan offer, adds another 3–7 days. The full process from eligibility check to DLD title deed typically runs 4–8 weeks for a straightforward ready-property purchase.

Can I get a mortgage for off-plan property in the UAE?

Some UAE banks offer mortgages on off-plan property, but it depends on the lender, the developer, and the construction stage. Most lenders require the project to be at least 50% complete before they will lend. Developer payment plans are commonly used in early construction phases, with a bank mortgage structured closer to handover.

What is the DLD mortgage registration fee?

The Dubai Land Department charges 0.25% of the mortgage value to register the mortgage. This is a fixed government fee, not negotiable, and cannot be included in the mortgage itself. It is paid at the DLD registration stage and is processed within 20–25 minutes at the DLD service centre.

Ready to Get Your Free UAE Mortgage Assessment?

Understanding how UAE mortgages work is one thing. Finding the right rate, lender, and structure for your income, residency status, and property type is another.

WhatsApp CityMortgage now at +971 50 925 5050 for a free, same-day eligibility assessment. We compare 25+ UAE lenders and find the right mortgage for your profile — with full transparency and zero obligation.